“The stock market is a device for transferring money from the impatient to the patient.”

- Warren Buffett

In only three months, 2024 has already been a notable year: the largest earthquake to hit New York City since 1884, a total solar eclipse that will not reoccur for another twenty years and both the Dow Jones Industrial Average and the S&P 500 reaching record highs during the first quarter. With the S&P 500 gaining more than 10% in the first quarter, it was the best start to the year since 2019.

The first quarter brought mostly welcome economic news. A variety of leading indicators showed the U.S. economy, which not long ago was widely expected to go into recession, performed better than expected despite meaningfully higher interest rates and still-elevated inflation. A strong consumer and labor market, the economy’s resilience, expectations that the Federal Reserve (Fed) will still cut rates this year (albeit less than the market had hoped) and enthusiasm surrounding artificial intelligence pushed stocks to new highs. Perhaps one of the most important trends we are seeing is a healthier level of breadth, which is to say: more stocks are participating in the rally. In 2023, the so-called “Magnificent 7” stocks were responsible for about 60% of the increase in the S&P 500. Now in 2024, all but one sector had positive returns in the first quarter (the highly interest-rate sensitive real estate sector declined). We believe this broader participation in returns is positive.

There has also been a significant divergence in the performance of the Mag 7 stocks, leading Wall Street to coin a new term, “Fab Four.” Nvidia, Meta, Amazon, and Microsoft continue to outperform the overall market.

We’re seeing support for additional gains in terms of earnings. In the first quarter, the S&P 500 notched its third straight quarter of year-over-year earnings growth, according to recent estimates. For the full year, analysts expect S&P 500 earnings to grow by nearly 11% over the prior year, which, if correct, would be roughly equal to the index’s historical annual rate of growth for earnings.

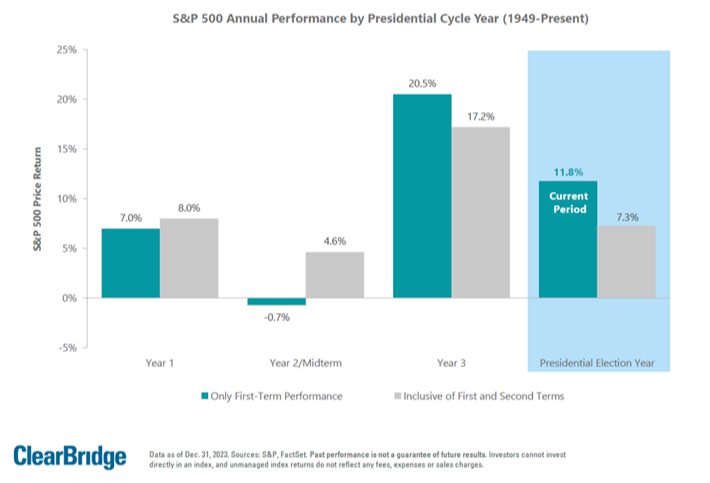

This year will also be historic because it is the largest global election year ever with more than sixty countries voting in presidential, legislative, or local elections. November’s U.S. Presidential election will be the first rematch since 1956 and offers two candidates with diametrically opposed policy paths. When it comes to the election, the good news is that its effect on the market is likely to be short-lived. Our analysis of historical data shows that volatility tends to be higher during election years, but the average rate of return on the S&P 500 is 11.8% since 1949 (see chart below).

One of the things that has become clear this year is that the Fed has been relying on the same policies that were successful in previous cycles, yet they have not been as effective this time around. Why is this happening? The post-pandemic economy is meaningfully different from the pre-pandemic period. Also, the U.S. economy today is dramatically different when compared to the late 1970s and early 1980s when the previous period of concerningly higher inflation occurred. Today, we are a service-based as opposed to a manufacturing-economy. A service economy is less capital-intensive and, therefore less impacted by changes in interest rates. Additionally, our economy is now supported by a larger number of government spending programs than in the past. Time will tell if the Fed begins to acknowledge these differences and considers disparate policy tools in the future.

In summary, the U.S. economy has shown remarkable resilience, and we expect it to continue to grow this year. That said, stubborn inflation, the presidential election, and geopolitical risks (namely the wars in Ukraine and Gaza) may contribute to increased volatility. As long-term investors, it is imperative to drown out the noise and focus on our plans. After all, the formula for all our work is: Your Goals à Your Plan à Your Portfolio. We don’t build your portfolios in contemplation of perfectly forecasting the economy or timing the markets (both of which are impossible); rather, they are the funding mechanism for your goals and are managed according to principles and practices that have never failed in the long run.

Thank you, as always for the trust you place in our team. It is an honor to be of service and walk alongside you in this life journey. If you have any questions or want to have a conversation, feel free to reach out anytime.

With gratitude,

Anne & Atricia