"Investing is not about timing the market, but about time in the market."

Performance Summary

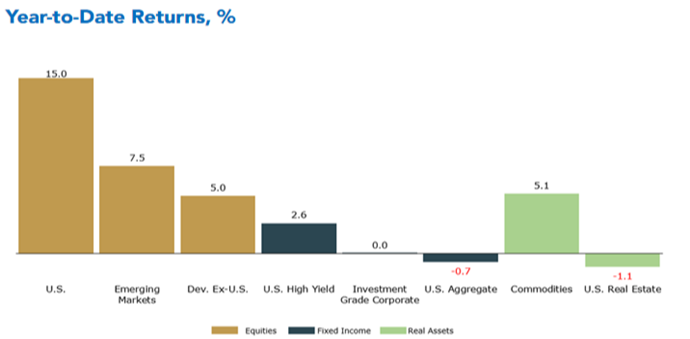

After posting strong returns in the first quarter of 2024, the S&P 500 index marked new highs in the second quarter, gaining about 5% for the quarter and 15% year-to-date. Gains came despite the Federal Reserve (the Fed) delaying interest rate cuts due to more stubborn inflation. The technology sector played a significant role in the stock market rally, contributing half of the index’s year-to-date earnings growth. Looking ahead, earnings growth will be key and elevated valuations (or how expensive stocks are) are a potential headwind.

Outside of the U.S., emerging markets returned 7.5% while developed international market stocks returned 5% YTD. The bond market continued to struggle as persistent inflation delayed interest rate cuts, which in turn supported commodity prices. Real estate continued to underperform as investors came to grips with “higher for longer” rates in a highly leveraged, interest-rate-sensitive sector.

Economy

Economic data has been mixed but generally strong. The U.S. added 206,000 jobs in June, however the unemployment rate increased to over 4% for the first time since November 2021, showing signs that the

job market is slowing. Consumers are also showing signs of moderate strain with increased credit card delinquencies, lower personal savings rates, and personal savings well below pre-pandemic levels. Consumer sentiment has also been at or below levels typically seen during recessions for much of the past two years, despite inflation having abated significantly. This may be because overall prices are still almost 21% higher since the pandemic-induced recession began in February 2020 according to the Bureau of Labor Statistics. For comparison, inflation rose 18.9% in the 2010s, 28.4% in the 2000s, and 32.4% in the 1990s. This recent inflation, experienced over just about four years, means that consumers need about $1,208 to buy the same goods and services that cost $1,000 when the pandemic began. Though the rate of inflation has slowed, consumers are unhappy with the overall increase. As a whole, the economy is in a late-cycle transition, characterized by slowing growth and potential for increased volatility.

Bull Market & Fed Pause

The current bull market, which began on October 12, 2022, is approaching its second anniversary and has gained 52.8%. That may sound like a lot, but it is actually a bit short of the historical average gain for a two-year-old bull market at 60% (Source: Factset). The Fed is currently on pause, defined by the time period between the last rate hike of a cycle and the first rate cut of the next cycle. The current Fed pause, at 331 days, is the second-longest in modern market history, trailing only 2006-07 (446 days), while the average of the six pauses since 1989 has spanned 248 days.

The S&P 500 has risen during five of these six pauses, with an average gain of 14.5%. The 2000-01 pause was the only one where stocks fell – the S&P 500 lost 7% during that pause, which was blemished by a recession and accounting scandals. Since the current pause began, after the Fed last raised rates on July 26, 2023, the S&P 500 has gained 20.5%. (Source: LPL Research, Bloomberg) Additionally, the S&P 500 had double digit gains in the 4th quarter of 2023 (11.2%) and the 1st quarter of 2024 (10.2%). This is only the ninth time since 1940 (84 years!) where the S&P 500 had double-digit gains in consecutive quarters. (Source: Nasdaq)

Volatility

Volatility is a normal characteristic of stock market investing. On average, in a given year, the S&P 500 index experiences three pullbacks (5-10%) and one 10-20% correction. The average maximum drawdown in a positive year, which 2024 will likely be, is 11%. So far in 2024, the maximum drawdown for the index has been just 5.5%, suggesting more volatility may be coming. The November presidential election will also loom large. Given the political uncertainty, we would expect volatility in the markets to begin to increase in late summer and early fall. That said, we are reminding clients that the market tends to do slightly better in election years than non-election years, so we would not recommend any large changes in anticipation of the election. During a presidential election year, increased volatility in September and October is common.

Looking to the back half of the year and beyond, lingering geopolitical uncertainty and an upcoming U.S. presidential election underscores the importance of diversification in a fundamentally uncertain world.

Through good markets and bad, our team remains committed to our collaborative partnership with you. We value our relationships and strive to provide the best possible guidance. It’s a privilege to be your trusted partner, and we appreciate the trust you place in our team. Thank you for allowing us to be of

service and walk alongside you in this life journey. If you have any questions, or want to have a conversation, feel free to reach out anytime.

With gratitude,

Anne & Atricia